Budgeting is telling your money where to go instead of wondering where it went – Dave Ramsey

Budget- we’ve all heard the word and we’ve all shuttered at the thought. Did you know that having a budget and getting in the habit of sticking to it can significantly reduce financial stress in your life? It may seem stressful to figure out the best way to budget and then keep it going. However, just knowing that having things ready when it’s time to write that check or click that “pay” button and not having to worry where its coming from creates a sense of success in your life and in your outlook.

But wait, how do you budget? There are so many different ways. How do you know which way is right for you? Simple….. no two budgets are identical. Because no two financial situations are identical. You find a basic budget (you’re in the right spot, there will be a couple different basic budgets highlighted throughout this bog) you start basic and adjust accordingly. Your budget may start as one way and end up as another as your financial situation changes over time. The overall goal is to be prepared when that time comes. Budgets are designed so that money is available when needed and to help add a cushion or better known as savings.

What is a Budget?

Quick, easy and simply put, a budget is a way to allocate where your money goes before it disappears. Its a plan for what you need/want to do with your money?

Why Should You Budget?

Budgeting helps you manage your spending habits, helps build better financial independence and freedom. Budgeting can help you get out of debt and help you save for emergencies or for large financial purchases without hurting your financial status. Budgeting can also help you manage your spending habits and help create a better financial grasp.

Where Do I Start?

Beginning to budget can feel overwhelming. Don’t fear it, embrace it. Using this very simple method for the 1st month, will allow you to help find the best budget for your situation.

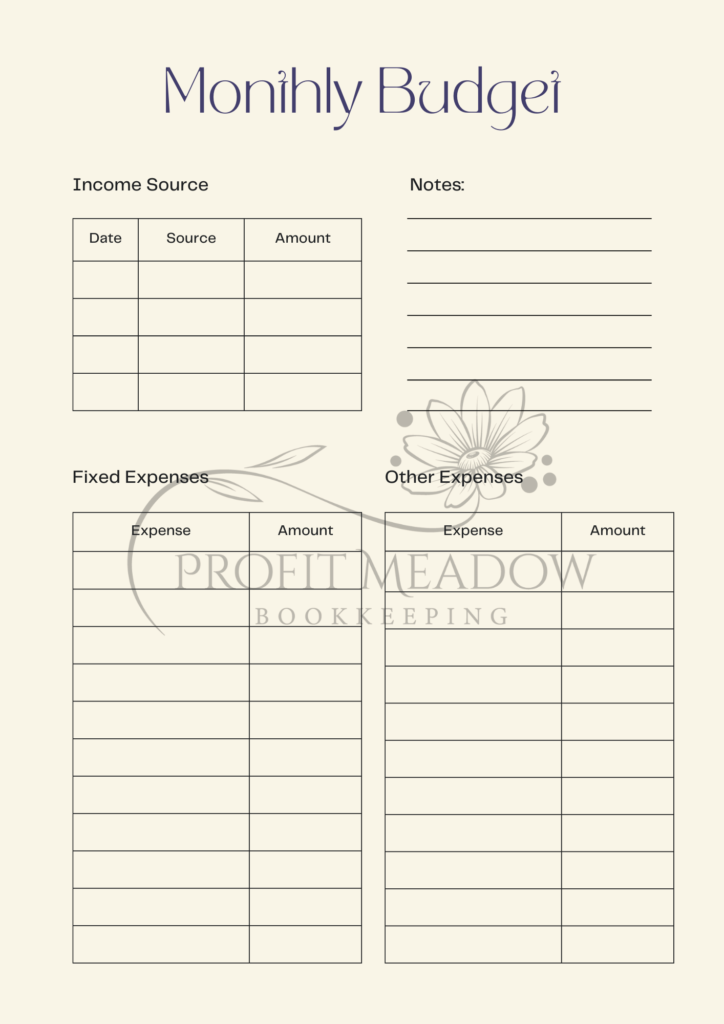

Figure your income (any money that you plan to get for the timeframe you are budgeting for)

List your expenses (this is any money that you expect to go out)

Subtract your expenses from your income

For the 1st month, track and list every single one of your expenses, categorizing these using labels such as food, utilities, shelter, transportation, household needs, dining out, wants, needs (these will be different for every household

At the end of the month tally everything up, decide what you want to spend in each category to create your new budget.

Picking a Budget Model

Now that you know how much you have coming and what you have going out, it’s time to find your budget model. A budget model is the framework for how you will manage your money. I will list a few that work great for beginners. It is important to remember that each budget model has its own pros and cons. you may start with one and transition to a different one several times before you find the right one for you. then as your financial status or situation changes, you may need to change agian. It’s ok, this is expected and quite frankly encouraged as you get better at managing your finances.

Zero Based Budget– This model starts with a clean slate each month. You will track every dollar and assure that it is being spent on your choice of categories. This does not mean that you have to spend it all, in fact I encourage challenging yourself to have more left at the end of each month than the last. If you tend to like to be in complete control of everything a control freak if you will, this may be a good option for you. The pros and cons of this budget model are pretty much the same thing, it depends on your preferences as to whether you see it as a pro or a con.

Pros-This can be very detailed and time consuming

Cons- Very detailed and time consuming

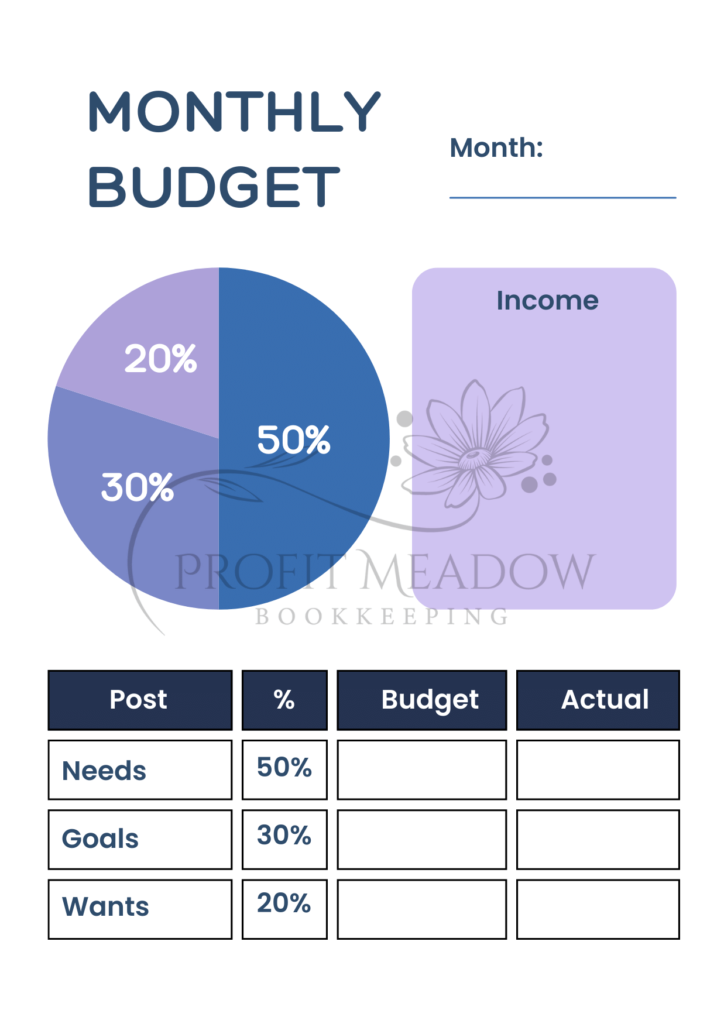

50/30/20 Budget- For this budget model you will allocate a certain percent of your income to each category. Simply put 50% towards needs (shelter, utilities, food, etc) , 30% towards goals (savings, 401k, vacation funds, etc), 20% towards wants (eating out, shopping, etc). This budget model leaves a lot of wiggle room.

Pros-This is a great way to be sure that an appropriate amount is going to the right categories, for instance if you get halfway through the month and realize your “wants” category is empty, then you may need to take a hard look at what you spend on wants and decide if they are hurting your financial situation.

Cons-For some the fact that this budget model is so simple can be a con. It makes it too easy to juggle money from one category to another. Too much wiggle room in your budget can lead to bad spending habits and taking from one category to cover another.

Envelope Budgeting- This budget model involves allocating a set amount of each income to envelopes, once that cash is gone, its gone until the next income date. This model requires you to know your expenses and divide the amount between each category in the appropriate amount to be sure that when the time for that category to be spent comes, the correct amount is there. This may involve averages that you use monthly. This model may be good for people who find themselves overspending then relying on credit cards to get to the next income date. This method involves cash. (Although you could allocate that to an account or multiple accounts, depending on how deatiled you want to be with this, but the concept is created to use cash)

Pros-Seeing the amount of money for a certain category can help you be more aware versus just swiping a card. This method can help you curb bad spending habits. You can choose how many envelopes you want to track. For instance, you can have one for utilities or you have one for electric, one for water, one for gas. This is your decision based on how detailed you want to be.

Cons- Cash may not be as secure as using a card. You must make sure you do not lose the envelopes.

Now You Can Start Your Budgeting Journey

Using the simple yet effect methods laid out in this blog, you can begin to budget. As you grow in your knowledge of your own finances and gain some understanding you will tweak the systems to work for you. Budgeting can be fun. I challenge you to start a savings challenge with yourself! This gives you a leg up so to speak as you research and track your expenses and income. There are a couple here that may be easy to start with. it can be very exciting to cross out the spaces and watch your savings grow! Be sure to watch this page a future blog about savings!